TechMagic Academy

TechMagic AcademyCyber Security in Banking: How We Address Rising Challenges

Last updated:11 March 2026

Financial institutions keep adding digital channels, connected services, and third-party tools. That creates more convenience for customers, but it also gives attackers more ways in. The IMF says the number of cyberattacks has almost doubled over the last 6 years, and nearly 20% of all reported cyber incidents affect financial firms.

For banks, the damage is rarely limited to IT. A cyber incident can interrupt payments, lock up internal systems, trigger compliance issues, and shake customer confidence. IBM’s 2025 Cost of a Data Breach Report puts the global average breach cost at $4.44 million, while Verizon’s 2025 DBIR shows that 30% of breaches involved a third party, twice the share reported a year earlier.

That is why cyber security in banking needs constant attention. Banks have to strengthen controls, monitor risk continuously, and keep pace with both regulation and the way attacks are changing. Strong protection now depends on more than individual tools. It depends on how well security holds up across the whole operation.

In this article, we look at the main cyber threats banks face today, the security measures that help reduce risk, and the practical steps financial institutions can take to strengthen protection.

Key Takeaways

- Cybersecurity in banking sector is getting more complex due to digitalization and expanding attack surfaces.

- Phishing, ransomware, and third-party vulnerabilities remain the most common risks in bank cyber security.

- Strong security requires both modern tools and continuous employee awareness.

- AI is improving detection but also enabling more advanced attacks in cyber security and banking.

- Banks that treat cybersecurity as an ongoing process are better prepared for future threats.

- Regulatory pressure continues to shape how cyber security for banking is implemented.

Latest Cybersecurity Threats in Banking

According to IBM, in 2025, the average cost of a data leak across all sectors in the United States reached $10.22 million U.S. dollars, the highest position worldwide. An average data breach in the financial sector hit $6.08 million U.S. dollars per incident, ranking the financial industry second based on the average cost of data breaches worldwide.

Financial institutions risk losing millions of dollars and reputation in case cyber attackers make use of system vulnerabilities. Let's take a closer look at the latest cyber threats.

Phishing attacks

Phishing remains one of the biggest threats in the cyber security banking industry. The financial sector is one of the most targeted by phishing scams. In 2024 Q4, almost 12% of phishing attacks worldwide targeted financial institutions. Phishers pose as legitimate banks or financial institutions. They target unaware people by sending fake forms, misleading emails, or messages containing malign links aimed to obtain sensitive information. The miscreants penetrate the network of a financial institution and can carry out a more significant attack aimed at data theft.

One of the common phishing tactics is creating a sense of urgency or panic. The attackers state that the account of a receiver has faced suspicious activity, or their information is required to be updated right away. The aim is to make users act without thinking critically. In 2026, attacks are much harder to detect because they use AI-generated content, making emails and messages more convincing than before.

Trojans and keyloggers

Banking trojans are a type of malware designed to target your online banking information. They act like a digital trojan horse, pretending to be legitimate applications while secretly deceiving you. Trojans imitate the appearance of your bank official login page. They intercept login details and codes within a banking session.

This misleading tactic plunges you in a bogus feeling of security, aiming to deceive you and steal your sensitive personal information. As soon as installed, banking trojans act like information vacuums and absorb your financial data. Trojans often implement the technique of keylogging, which records all the information you type, such as usernames, passwords, and one-time codes.

Malware

Malware, or malicious software, intends to obtain sensitive financial information, such as account numbers or passwords, and violate financial transactions. Malicious software poses a considerable cybersecurity threat in the banking sector due to its ability to implement various methods to break through security measures and infect devices.

Join our upcoming webinar to get practical guidance before your next audit

Ransomware

In 2025, 62.6% of businesses worldwide were affected by ransomware attacks. Thus, they remain a major risk for cybersecurity for banking. Ransomware is a type of malware that targets the data of a user or organization, taking it hostage and demanding a ransom charge for its release. In the banking sector, ransomware attacks are especially harmful as they disrupt financial operations and put confidential financial information at risk.

Ransomware can encrypt critical data, such as customer information, financial records, and transaction details. This encryption renders the data unreadable and inaccessible, and locks the bank out of its own data. With critical data locked away, crucial operations like processing transactions, accessing customer accounts, and even internal communications can become impossible.

The potential reputational and financial losses put banks under the pressure to pay the ransom to recover bank activity rapidly. According to Cybersecurity Ventures prediction, ransomware will cost its victims around 265 billion U. S. dollars annually by 2031.

Third-party risk

Third party integrations boost the efficiency for banking institutions, but they also introduce significant cybersecurity vulnerabilities. Every third party system a bank connects to creates a new entry point for attackers. Weaknesses in a third party security can be exploited to get access to the network or data of financial firms. In 2026, cybersecurity in banking sector must include strict third-party risk management, as many breaches now originate from vendors, APIs, or external platforms. At TechMagic, we integrate cybersecurity services, making sure that all the implemented safeguards work properly and nothing endangers the system.

AI-related cyber threats

Artificial intelligence enriches the cybersecurity in banking market, with notable advancements in fraud monitoring, risk management, and customer support. At the same time, AI-related technologies create the ground for new security threats. AI is empowered to develop synthetic media, such as realistic fake videos or audio, known also as deepfakes. Cyber attackers implement deepfakes to pretend to be bank representatives in social engineering attacks and approach your personal details and information. Attackers can now scale social engineering campaigns faster and with higher success rates.

Remote workforce

Remote work has become the norm in many spheres of activity, including the banking sector. Still, when a remote worker has access to important or sensitive information, there are additional risks associated with data breaches. Remote work creates potential cyber threats as unsecured networks, weak endpoint security, and physical security concerns. This expands the attack surface, especially when access control and endpoint protection are not properly managed.

Distributed denial of service

A DDoS attack is a cyberattack that overloads a system with traffic. This prevents legitimate users from accessing their accounts, making transactions, and contacting customer support. For banks, even short disruptions can affect thousands of users at once and lead to immediate financial and reputational impact.

Data breaches

Unencrypted data stored in a device of a bank is the root of many potential threats. If your data is unencrypted, in case of a breach hackers can easily access all the sensitive data and use it against you and your customers. In many cases, breaches are caused by simple gaps like misconfigured storage or weak access controls.

Let's Explore Real Cases: Top Cybersecurity Attacks on Financial Institutions

Digital transformation has restructured the way we manage our finances. Online banking and mobile payment apps provide users with convenience, but they also set the basis for new vulnerabilities to arise in financial systems. Over the last 5 years, 863,000 cyber crimes were reported in the US annually, accorsing to the FBI’s Internet Crime Complaint Center.

Cybercriminals are continuously inventing sophisticated formulas and approaches to make use of these weak points and attack financial institutions and their customers. In 2026, incidents show that attackers rarely rely on a single method. Most breaches now combine phishing, credential theft, and system vulnerabilities, which makes prevention more complex.

Let's have a look at recent cyber attacks on financial institutions to get a wider perspective on the complex strategies used by attackers and the destructive consequences they may result in.

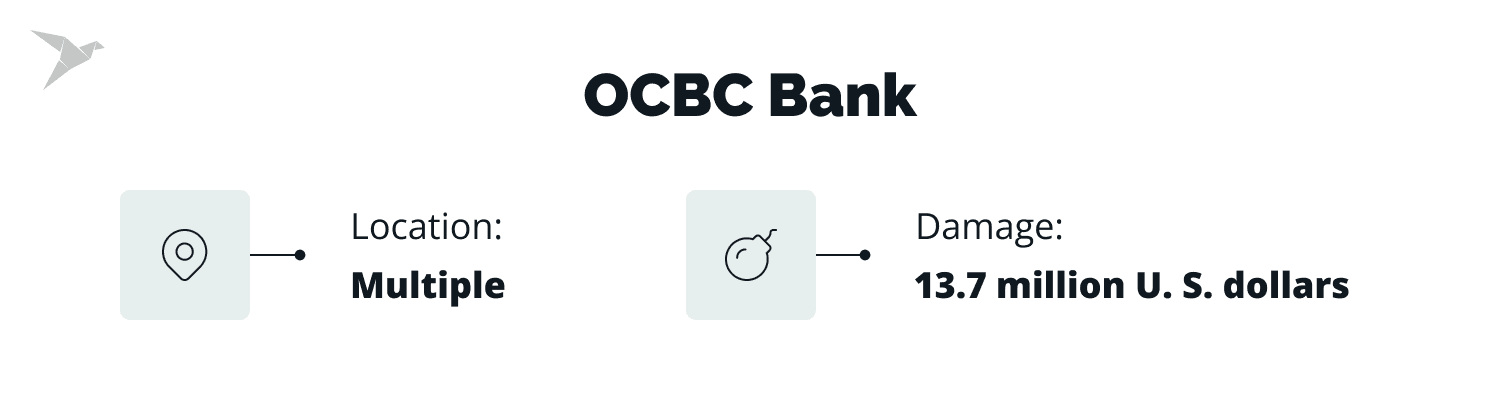

$13.7 million OCBC phishing scam

On December 23, a phishing scam targeting the Singaporean bank OCBC resulted in a loss of 13.7 million U. S. dollars. Approximately 790 banking customers fell victim to the incident. Affected persons received untruthful messages claiming that there were issues with their banking accounts, asking them to click on a link to solve the problem.

After clicking, victims were redirected to fake bank websites and demanded to type in their account login information. As soon as they clicked on the phishing link, attackers got an opportunity to log in to the bank account of a victim and withdraw all funds from it. Affected people would realize they had been scammed once they got messages from a legitimate bank notifying them of unauthorized transactions charged to their bank accounts.

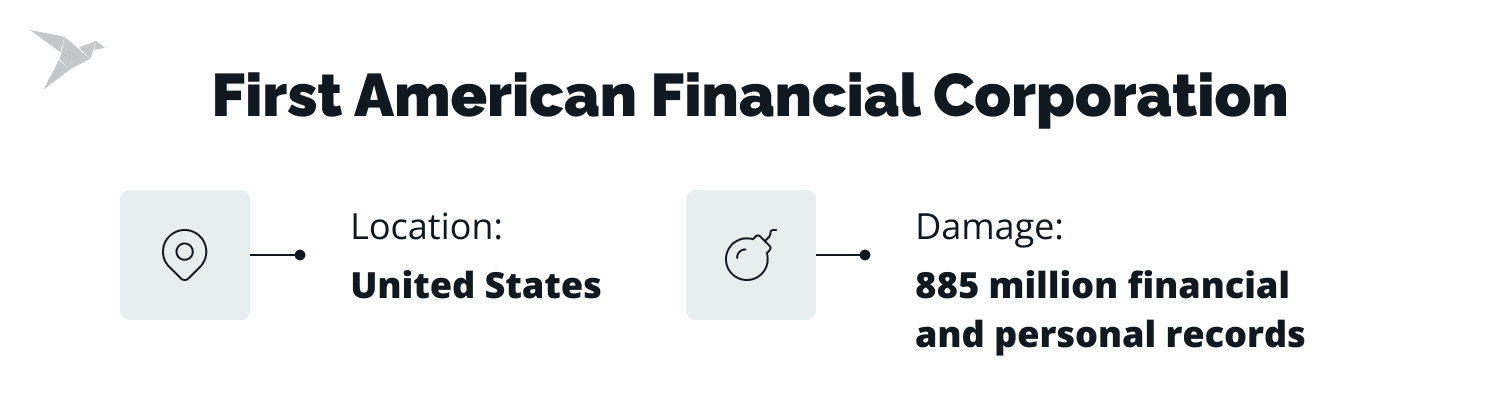

885 million files First American Financial Corp. data breach

On May 24, First American Financial Corporation faced a data breach involving up to 885 million financial and personal records linked to real estate operations. The documents, dated back to 2003, were exposed as a result of a common website design error. The breached data included bank account information, mortgage and tax records, driver licenses images, social security numbers, and other sensitive information.

A web page link giving access to sensitive data was not secured by a multi-factor authentication policy. Anyone with access to at least one document link could approach others by changing the figures of a record number. The company shut down the website, but a lot of the pages were still accessible on the archive websites. Such personal details as names, email addresses, agents and buyers mobile phone numbers were compromised. With this information, it is possible to commit such cyber crimes as identity theft, malware injections, and ransomware attacks.

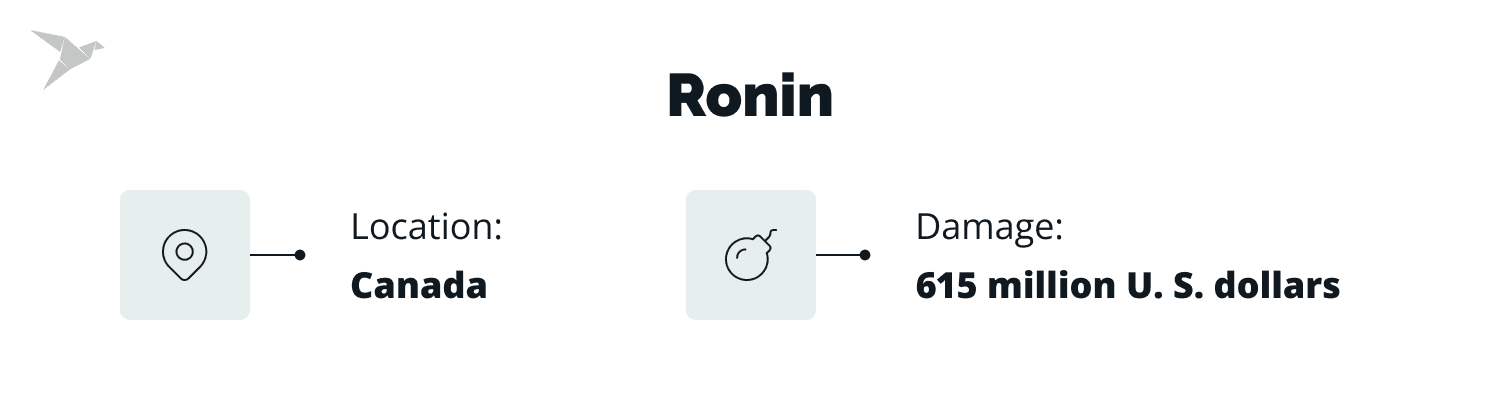

$615 million Ronin cryptocurrency theft

On March 23, blockchain project Ronin lost 615 million U. S. dollars due to a cyber attack. Cyber attackers exploited a function enabling users to transfer their digital assets from one crypto network to another one. It is thought to be the second-largest cryptocurrency theft. Ronin mentioned that the hacker had used stolen private passwords required to access crypto funds to get hold of them. The United States assigned the cyber attack to the North Korean state-backed hacking collective Lazarus Group and imposed new sanctions against them.

Risk Awareness

Customer information disclosure can lead to harmful consequences, such as:

- Identity theft

- Scam transactions

- Account draining

- Unauthorized charges issues

- Fraudulent money transfers

These deceitful activities not only result in direct financial expenses for the bank but also require costs for investigations, remediation, and compensation to customers. In addition to instant financial losses, banking institutions must deal with regulatory and compliance penalties for non-adherence to policies to keep customer data safe.

Despite the financial harm, the reputational damage after a cyber attack usually appears to be catastrophic. Loss of customer trust is often the most expensive outcome. Customers expect banks to protect their data, and even a single breach can impact long-term relationships.

The effect on customers can be no less destructive. A data leak results in significant financial losses for individuals. Accounts opened in their name can leave them saddled with debt, while unauthorized transactions can drain their savings.

The evolving nature of cyber threats further intensifies the challenge. Hackers are constantly innovating and developing new methods to exploit vulnerabilities in security systems. Phishing emails become more sophisticated, malware disguises itself better, and social engineering tactics become more convincing. This constant evolution necessitates a proactive approach from banks.

Cybersecurity Solutions for Efficient Protection

Advanced security solutions help banks to succeed in maintaining a robust security system. Strong cyber security for banks relies on layered protection. Let's have a look at the key ones.

Data encryption

Data encryption encodes sensitive information such as personal profile details or social security numbers. This process makes the data unusable for anyone who doesn't have the decryption key. Encryption minimizes the damage caused by such attacks and builds customer confidence by prioritizing data security.

Multi-factor authentication

MFA serves as an additional security measure for online and mobile banking. Beyond just a password, MFA necessitates another confirmation step, such as a code received on your phone or a fingerprint scan. This notably impedes unauthorized access, even if hackers manage to steal your password. With MFA, it becomes considerably more difficult for criminals to pretend to be you and gain access to your financial information.

AI-driven threat detection

AI-driven threat detection systems meticulously analyze massive datasets to identify unusual activity in real-time. AI can detect and respond to cyberattacks with greater speed and efficiency as it recognizes patterns and inconsistencies that might elude traditional methods. This empowers banks to prevent potential breaches before they occur. Modern systems focus on real-time monitoring instead of periodic checks, which reduces response time and limits damage. Additionally, considering penetration testing pricing can help financial institutions evaluate the cost of proactively identifying vulnerabilities before they can be exploited.

Regulatory Compliance

A system of regulations has been established to safeguard consumers and decrease security weaknesses in the banking system. Financial organizations must be aware of these crucial requirements to act legally and in a secure way. In fact, regulation plays an essential role in cyber security in banking.

Adhering to cybersecurity regulations and standards is not only about avoiding penalties. It proves the loyalty of a bank to protect customer data and maintain a secure environment. Strong cybersecurity practices build trust with both customers and regulators, which results in a more secure and stable financial system.

These standards often manage data security safeguards, risk assessments, robust protocols for customer data privacy and protection, as well as constant system monitoring and incident reporting. Requirements are becoming stricter, especially around data protection, incident reporting, and third-party security.

Government regulations

On a global scale, governments take action by enacting laws that require banks to implement specific cybersecurity practices. These regulations can dictate various aspects of data security, including what needs to be protected, how to handle breaches, and how personally identifiable information privacy is safeguarded. Examples include the Gramm-Leach-Bliley Act (GLBA) in the United States and the General Data Protection Regulation (GDPR) in the European Union.

Financial industry standards

Beyond general regulations, financial institutions face additional cybersecurity guidelines. These detailed standards, often created by industry groups in collaboration with regulators, outline specific technical controls, risk management strategies, and how to respond to security incidents. Managed SOC pricing can help financial institutions meet regulatory compliance by offering the tools and expertise needed for continuous monitoring and effective incident response.

Cybersecurity framework examples include:

- NIST Cybersecurity Framework

- North American Framework for Financial Services

- CIS Critical Security Controls

- SOX

- GLBA

- PCI DSS

- ISO 27001/27002

- The Bank of England CBEST Vulnerability Testing

Investment in Cybersecurity

According to Gitnux Marketdata report, cybersecurity investment in the financial services sector is predicted to reach 68.3 billion U. S. dollars by the next year. Financial investments in cybersecurity measures is an essential component of a successful and safe banking system.

Investment in cybersecurity awareness keeps banks ahead by keeping up with the latest cybercrime updates and knowledge. Banking organizations reinforce their systems by teaching employees to detect and resist cyberattacks. Infrastructure modernization strengthens the digital perimeter of a bank against evolving threats. This multi-layered approach safeguards sensitive data, fosters trust, and minimizes financial expenses. Considering cybersecurity as a strategic investment results in long-term prosperity and solidity for financial firms.

Employee Training and Awareness

The battle against cybercrime starts with employees in your bank. They learn to detect scam like phishing emails and malware and eliminate them before they result in destructive consequences. Regular training enhances a security-minded culture where employees use strong passwords, treat data responsibly, and report suspicious activity immediately.

Human error is still one of the leading causes of breaches, which makes training just as important as technology investments. Keeping employees informed of the latest threats minimizes human error and protects sensitive customer details. Investing in employee awareness is a powerful shield against cyberattacks.

Here are some ways to maintain employee awareness:

- Engaging regular security awareness training

- Keeping employees informed about the latest cyber threats

- Conducting phishing and other cyber threat simulations

- Reporting mechanisms policy implementation

Citigroup: Continuous Monitoring and Employee Training

A showcasing example of a successful security safeguards implementation in the banking system is the story of Citigroup. Citigroup, a leading financial services giant in the USA, has employed a sophisticated cybersecurity strategy that prioritizes constant monitoring, threat competence sharing, and employee awareness training. The complex approach and proactive role have led to notable success in protecting confidential data and mitigating cyber threats.

Key elements of Citigroup successful strategy

Advanced security monitoring: Citigroup uses security systems to continuously monitor network activity for suspicious behavior. This helps with instant threat detection and potential cyberattacks reaction.

Threat intelligence sharing: Citigroup takes part in field-wide threat knowledge sharing initiatives. This collaboration allows them to keep up with the latest cyber threats and vulnerabilities and adapt to defenses in a dedicated way.

Employee awareness training: Citigroup invests in cybersecurity awareness training for its employees. Regular training sessions equip employees with the knowledge and skills to identify phishing attempts, social engineering tactics, and other cyber threats.

The story of Citigroup demonstrates an example of a multi-layered cybersecurity strategy effectiveness in banking. Their never-ending monitoring, collaborative threat knowledge sharing, and commitment to employee training have reduced their cyber risk profile.

Get Ready for Future Cyber Threats

Cyber security in the banking sector demands constant attentiveness. New risks occur together with technological progress, so being aware of their potential impact is vital. Let's have a look at the potential risks of the cyber security future:

AI cyber threats rise

Cybercriminals use AI to personalize and automate attacks. These mechanisms can make use of vulnerabilities, create persuasive phishing emails that deceive filters, and even run extensive attacks at breakneck pace. Financial organizations have to resist this threat with robust AI-powered defenses able to detect and mitigate emerging threats.

Supply chain risks

Cybercriminals are expected to actively attack third-party vendors and partners of financial organizations. They exploit security weaknesses in the systems and obtain access to the network or data of a bank. This emphasizes the crucial necessity for third party risk management.

Deepfakes advancement

Deepfake technologies are progressing into a serious problem for banking. Banks are required to implement staff training on deepfakes detection and implement reliable multi factor authentication policies to confirm transactions.

Conclusion and How TechMagic Can Help

Combating cybercrime demands a united interaction. All financial institutions, government agencies, and cybersecurity firms collaborating together build a more resilient financial ecosystem. Shared threat knowledge and valuable insights results in early detection of attacks. Open communication about best practices enhances all financial organizations.

Banks today have to resist a progressive number of cyber threats. Luckily, there is a clear picture of how to act to keep your banking experience absolutely secure. Solid safeguards, employee training, and the overall security culture are the key ways to reach a robust security posture.

At TechMagic, we help financial institutions build practical cyber security for banking strategies that match real systems, real risks, and real business goals. Contact us for a free scope consultation!

FAQ

Strong cyber security in banking sector is vital to safeguard sensitive financial data and prevent scam activity. Effective banking cybersecurity ensures data integrity, protects transactions, and supports financial stability for both banks and their customers.

Financial institutions often face such threats as phishing, malware infections, ransomware, unencrypted data breaches, unpatched vulnerabilities, supply chain attacks, DDoS attacks, trojans, and AI-related risks. These risks continue to evolve, making cyber security in banking industry more complex and demanding.

Banks deal with potential threats with a multi-layered approach that includes investing in advanced security systems and employee training, as well as collaboration with other organizations. This helps strengthen cyber security for banking and improves the ability to detect and respond to threats faster.

There is a wide list of regulatory requirements depending on the field peculiarities. Some examples include such frameworks as NIST Cybersecurity Framework, North American Framework for Financial Services, CIS Critical Security Controls, SOX, GLBA, PCI DSS, ISO 27001/27002, The Bank of England CBEST Vulnerability Testing, and others. These standards shape how cybersecurity in banking sector is implemented and monitored.

Banks invest billions of dollars in cyber security. Statista predicts that the global cybersecurity market size is forecast to grow to 538.3 billion U.S. dollars by 2030. This reflects the growing importance of cybersecurity in banking market and the need for continuous investment.

Collaboration and information sharing in cybersecurity empower financial institutions to detect threats faster through interaction, build powerful protections, and set a more solid defense against cyber attacks.

Bank employees can introduce a crucial power of financial cybersecurity defense if they stay watchful, identify phishing attempts, and comply with security policies to resist data leaks.

To make banking institutions cyber secure, it is essential to stay ahead of threats by following a proactive approach that combines constant monitoring, knowledge sharing, risk analysis, and employee training.