TechMagic Academy

TechMagic AcademyHow Should FinTech CTOs Choose a Cloud Services Provider?

Last updated:16 January 2026

Time is money in FinTech–and your cloud choice can quietly drain both. A single hour of downtime can cost millions. A poor compliance setup can delay market entry by months. Yet many CTOs still approach cloud selection as a technical checkbox, not a strategic risk decision.

This is why FinTech choosing a cloud services provider is no longer just about compute power or pricing tiers. It’s about how well your infrastructure supports regulatory pressure, handles transaction spikes, protects sensitive data, and scales without locking you into painful trade-offs. The wrong choice shows up later as audit friction, rising costs, or brittle systems that slow teams down.

In this article, we break down how leading FinTech companies approach FinTech choosing a cloud provider in practice. You’ll see how AWS, Azure, Google Cloud, IBM Cloud, and Oracle OCI differ where it matters most for financial platforms. We also share direct guidance from TechMagic’s FinTech leadership on how CTOs evaluate risk, scalability, and long-term dependency before committing.

Key takeaways

- Cloud provider choice directly affects regulatory readiness, uptime risk, and speed of expansion.

- Hyperscalers and enterprise clouds solve different FinTech problems and growth patterns.

- Security, data residency, and audit controls vary more between providers than most teams expect.

- Long-term cloud lock-in impacts pricing flexibility and future architecture decisions.

- The “best” cloud depends on your product model, not market share alone.

Why Is Cloud Provider Choice Critical for FinTech Companies?

FinTech platforms operate under tighter constraints than most digital products. Regulatory oversight, data risk, and uptime expectations directly affect revenue and trust. Choosing among the best platforms for FinTech cloud requires alignment with these pressures, not just general cloud capabilities.

Regulatory and compliance pressure in financial services

Financial services face strict requirements around data residency, auditability, and operational controls. Regulations often vary by region and change over time, which affects how infrastructure must be configured and monitored.

A cloud provider must support compliance through certified services, detailed logging, and clear responsibility boundaries. Clear service level agreements and shared ownership models are critical factors here. Gaps in these areas increase audit risk and slow product expansion into new markets.

Financial impact of downtime and service disruptions

Downtime in FinTech carries an immediate cost. Failed transactions, delayed settlements, or unavailable customer accounts lead to direct revenue loss and regulatory scrutiny.

Cloud providers differ in their availability guarantees, regional redundancy options, and incident response transparency. These differences matter when uptime expectations approach continuous operation and when teams must scale without compromising performance.

Data sensitivity and risk management

FinTech systems handle payment data, identity records, and transaction histories. Exposure or loss of this data creates legal, financial, and reputational consequences.

Provider-level controls for encryption, access management, and monitoring shape the overall risk profile. Robust security features reduce the burden on internal teams and make it easier to standardize controls across environments. Weak defaults or limited visibility increase the burden on internal teams and raise operational risk.

Long-term strategic dependency on cloud

Cloud choices create long-term dependencies. Data services, managed databases, and security tooling can be difficult to replace once deeply integrated.

For FinTech companies, this dependency affects pricing flexibility, geographic expansion, and regulatory response speed. Provider selection should account for exit options, interoperability, and long-term operating models, not only short-term delivery speed, especially when these critical factors influence future architecture decisions.

AWS: The Leader in Cloud Computing Services

Amazon Web Services (AWS) is a leading public cloud provider with a large global footprint and an extensive service portfolio. As of 2025, the AWS Cloud spans 38 geographic regions and 120 availability zones, with additional regions and zones announced for future expansion.AWS's market dominance is seen in its widespread adoption among various industries.

AWS remains a dominant player in the cloud market. In 2025, AWS held approximately 30 % of the global cloud infrastructure market, followed by Microsoft Azure at around 20 % and Google Cloud at about 12 %. It also delivers broad product coverage, with over 200 fully featured services across computing, storage, databases, networking, analytics, machine learning, and more

In its 2024 financial results, AWS generated approximately $107.6 billion in annual revenue, reinforcing its central role in Amazon’s business and in enterprise cloud adoption.

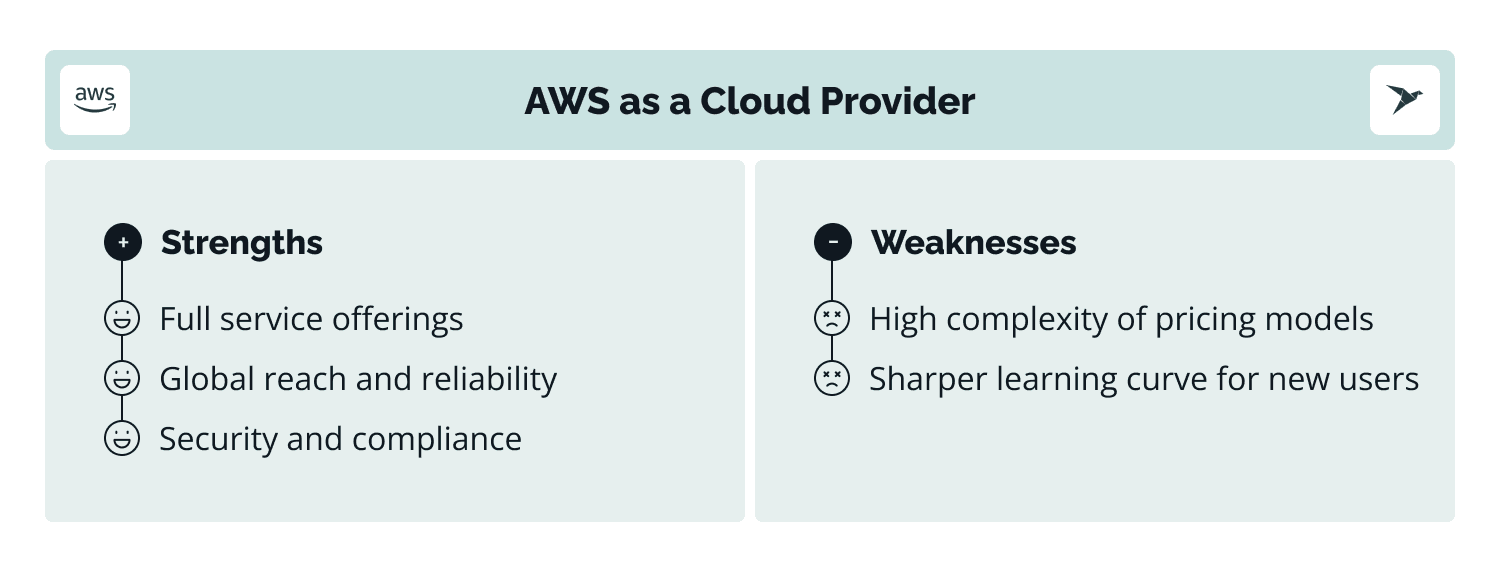

Strengths of AWS as a cloud provider

Let’s see what makes Amazon Web Services a top choice for cloud computing.

- Full service offerings. AWS offers an impressive set of tools and services that meet almost every cloud computing need. This involves compute power (EC2), storage solutions (S3), database services (RDS), and advanced analytics tools (Redshift). As of 2024, a total of over 41,000 products and services are offered on the Microsoft Azure marketplace, of which more than 2,800 belong to AI and ML services and products.

- Global reach and reliability. With a presence in 26 geographic regions and 84 availability zones, AWS ensures your applications are accessible to users worldwide while minimizing response times. The AWS network ensures low latency, high availability, and fault tolerance, crucial for sensitive industries like FinTech. AWS's access controls and data centers are constantly innovated to be protected from man-made and natural risks

- Security and compliance first. Data security is paramount, especially in finance. AWS boasts robust security measures and has earned trust through a wide range of compliance certifications, some of them are PCI-DSS, GDPR, HIPAA. AWS safeguards information with data encryption and prevents cyberattacks with DDoS protection.

Weaknesses of AWS as a cloud provider

Being aware of AWS’s strong sides, let’s explore its weak points to get a full understanding.

- High complexity of pricing models. The pricing structure of AWS can be too complex and confusing, especially for new users. The pay-as-you-go model, reserved instances, and various pricing tiers necessitate attentive monitoring to prevent unforeseen costs.

- Sharper learning curve for new users. The number of services and features can be overwhelming for those who are new to cloud computing. Proper training and expertise are needed to use all AWS's options available.

Stripe: a FinTech company using AWS

Stripe is a leading financial technology enterprise specializing in payment processing. Its operations are heavily dependent on Amazon Web Services for its fundamental cloud infrastructure.

Stripe handles millions of transactions daily, which necessitates a robust and scalable platform. AWS provides the essential groundwork for managing such substantial transaction volumes.

To oversee its computational data storage requirements, Stripe utilizes Amazon Elastic Compute Cloud (EC2). Delicate data is securely preserved on Amazon Simple Storage Service (S3). For efficient database administration, Stripe relies on Amazon Relational Database Service (RDS).

Given the sensitive nature of transactions, security is paramount. AWS offers proven security characteristics and has acquired numerous compliance certifications, which ensure the protection of Stripe's customer information.

Stripe relies on AWS's machine learning capabilities, which allow it to analyze vast transaction datasets to detect and prevent malicious activity. AWS's global infrastructure is necessary for Stripe. It enables uninterrupted service for clients all around the world.

This use case highlights the high potential of cloud computing in the FinTech industry.

Azure: Smooth Integration with the Microsoft Environment

Microsoft Azure is another leader among top cloud service providers. Microsoft Azure is widely chosen by enterprises that already use Microsoft technologies, such as Microsoft Entra ID, Windows Server, SQL Server, and .NET, because these integrations reduce friction across identity, governance, and management layers.

Azure’s cloud business has continued to grow strongly through 2025. In Microsoft’s fiscal year 2025 results, Azure and other cloud services drove growth in the Intelligent Cloud segment, with cloud revenue increasing notably year over year and Azure exceeding $75 billion in annual revenue, up around 34 % from the previous year. This reflects ongoing enterprise adoption and demand for cloud and AI-driven workloads.

On market share, industry analyses show Azure holding around 20 % of the global cloud infrastructure market in 2025, behind AWS but ahead of most competitors, with continued expansion in enterprise deployments and AI-related services.

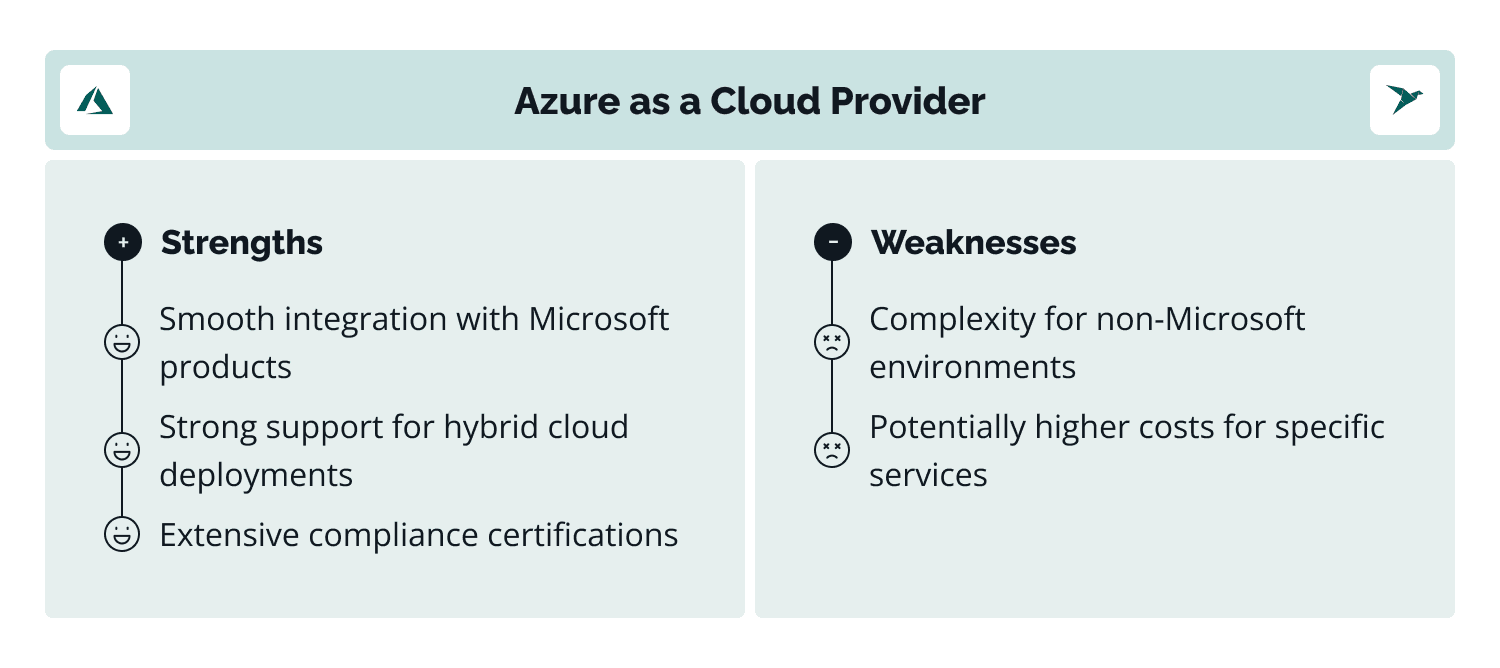

Strengths of Azure as a cloud provider

Let’s explore what benefits make Azure a preferred cloud services provider for organizations.

- Integration with Microsoft products. Azure integrates easily with Microsoft products, such as Office 365, Dynamics 365, and Active Directory. This fact results in a unified and effective user experience, especially beneficial for organizations which greatly invested in Microsoft technologies.

- Strong support for hybrid cloud deployments. Azure excels in hybrid cloud solutions. It enables businesses to combine on-premises and cloud environments. This flexibility is advantageous for FinTech companies possessing existing on-premises infrastructure seeking to transition to the cloud progressively.

- Extensive compliance certifications. Azure has many compliance certifications, such as GDPR, ISO/IEC 27001, and SOC 2. Such compliance support makes Azure a trusted choice for a highly regulated industry like FinTech.

Weaknesses of Azure as a cloud provider

Still, businesses that choose Azure as a cloud services provider may face some challenges:

- Complexity for non-Microsoft environments. Businesses not using Microsoft products might find Azure's environment less intuitive and more challenging to integrate with their existing systems.

- Potentially higher costs for specific services. Certain specialized services on Azure may incur higher costs than those of competitors. This requires careful cost analysis and management.

JPMorgan Chase: a FinTech company using Azure

JPMorgan Chase, a worldwide financial services innovator, has embraced Microsoft Azure as a critical element of its technology strategy. The bank uses Azure across various operations, including trade handling, risk modeling, client relationship management, and compliance operations.

Advanced analytics and AI capacities within Azure empower JPMorgan Chase to acquire profound insights, optimize strategies, and provide personalized financial offerings. Azure's robust security safeguards protect delicate data.

Azure's worldwide presence supports the bank's international operations. Through Azure, the bank shows how traditional financial institutions can transform into dynamic FinTech entities.

Still, the bank faced some challenges like data transfer, cost control, security, and integration with legacy systems, which needed considerable investments in time and resources.

Despite some difficulties, Azure remains a vital component of JPMorgan Chase's technology infrastructure, supporting various crucial business functions. The bank's incorporation of Azure's blockchain platform, Quorum, emphasizes a proactive approach to exploring distributed ledger technology for transforming financial processes and enhancing security.

Learn about our expertise in the industry and what we have to offer

Google Cloud Platform: Advanced Technology and Data Analytics

Google Cloud Platform (GCP) is next on this list of top cloud providers. GCP is known for its innovative cloud technology, particularly in data analytics and machine learning. About 960,000 businesses use Google Cloud Platform cloud computing solutions. Let's see what benefits GCP has.

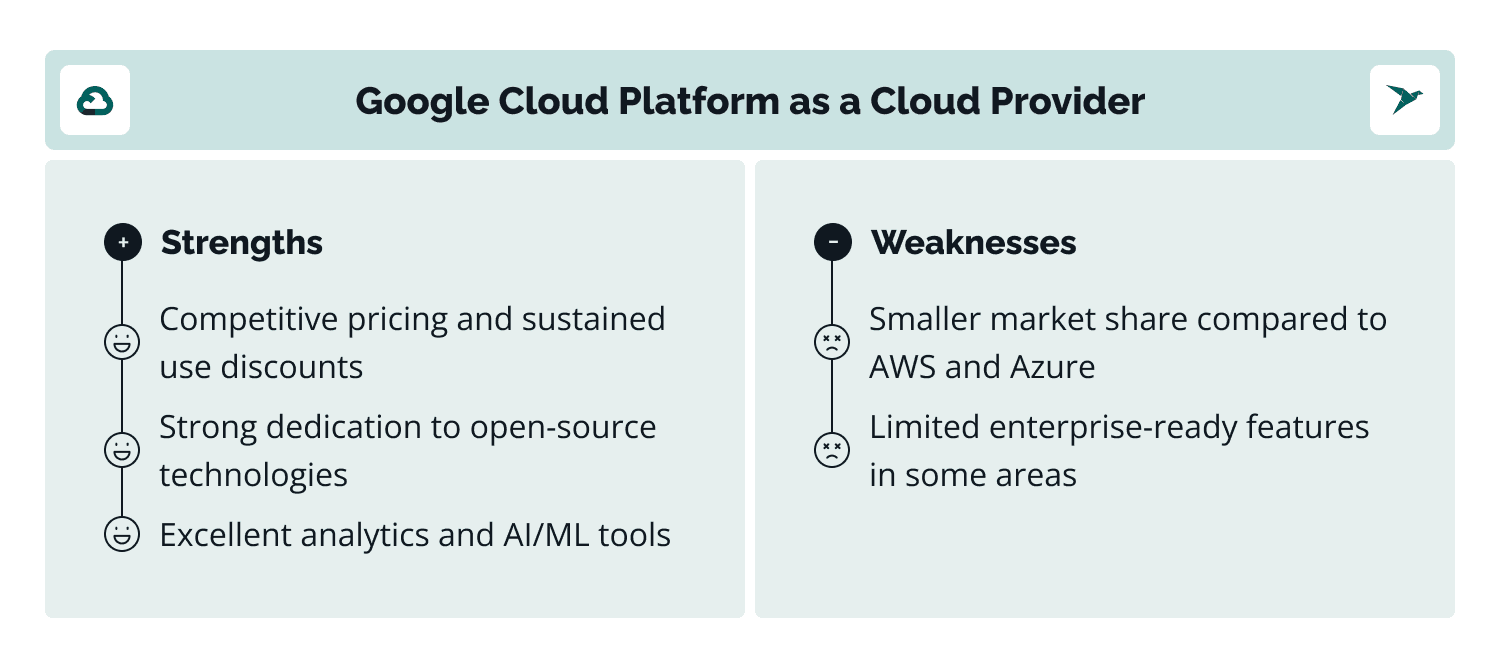

Strengths of GCP as a cloud provider

- Excellent analytics and AI/ML tools. GCP succeeds in data analytics and AI/ML as it offers powerful tools such as BigQuery, Dataflow, and TensorFlow. These tools enable FinTech companies to process huge amounts of data and build complex machine learning models.

- Competitive pricing and sustained use discounts. GCP provides competitive pricing with sustained use discounts, offering cost-efficiency for long-term usage. This pricing model helps FinTech companies manage their cloud expenditure effectively.

- Strong dedication to open-source technologies. GCP supports a wide variety of open source technologies. This devotion is especially attractive to tech-savvy FinTech companies.

Weaknesses of GCP as a cloud provider

- Smaller market share compared to AWS and Azure. GCP has a smaller market share, which might raise concerns about long-term viability and ecosystem maturity compared to AWS and Azure.

- Limited enterprise-ready features in some areas. Certain enterprise features on GCP might not be as mature or comprehensive as those offered by AWS or Azure, requiring additional third-party integrations.

PayPal: a FinTech company using GCP

PayPal, a foremost worldwide online payment system and digital wallet, uses the power of Google Cloud Platform. With GCP, PayPal extended its operations to serve millions of customers globally, process billions of transactions, and drive advancement in the payments industry.

GCP's robust infrastructure supplies PayPal with the scalability and dependability needed to manage the immense quantity and speed of payment dealings. Employing GCP's data analytics abilities, PayPal can derive valuable insights from transaction data, enabling data-driven decision-making, fraud avoidance, and customized customer experiences.

Moreover, GCP's artificial intelligence and machine learning tools empower PayPal to develop complex fraud detection models, which improve risk management plans and optimize payment processing workflows.

GCP's worldwide network helps PayPal guarantee low-latency dealings and smooth user experiences for clients worldwide. PayPal's strategic acceptance of GCP has been crucial in its evolution from a conventional online payment platform to a leading-edge financial technology firm.

IBM Cloud: Enterprise Focus and Regulated Workloads

IBM Cloud is positioned around hybrid cloud solutions, enterprise workloads, and integration with legacy systems. Its services combine infrastructure (IaaS) and platform (PaaS) offerings designed to support mission-critical applications with security and compliance controls across public and private environments. IBM Cloud operates globally through more than 60 data centers in 19 countries and multiple multizone regions.

Unlike hyperscalers such as AWS, Azure, or Google Cloud, IBM’s cloud revenue figures and exact market share are not always broken out publicly in the same way. However, industry data estimates that IBM holds a small share of the global IaaS/PaaS market (around ~2 % in 2025), with hybrid-oriented offerings and traditional enterprise integration services contributing to its presence outside the top three.

In terms of business performance, IBM’s overall revenue, including software, consulting, and infrastructure, has continued to grow through 2025. In Q3 2025, the company reported 17 % growth in its infrastructure segment year over year, with hybrid cloud and AI demand cited as drivers of momentum.

IBM is also investing strategically in cloud-related capabilities. In late 2025, the company announced an $11 billion acquisition of Confluent, a real-time data streaming platform aimed at bolstering its data and AI infrastructure offerings, which could expand IBM’s appeal in complex enterprise environments.

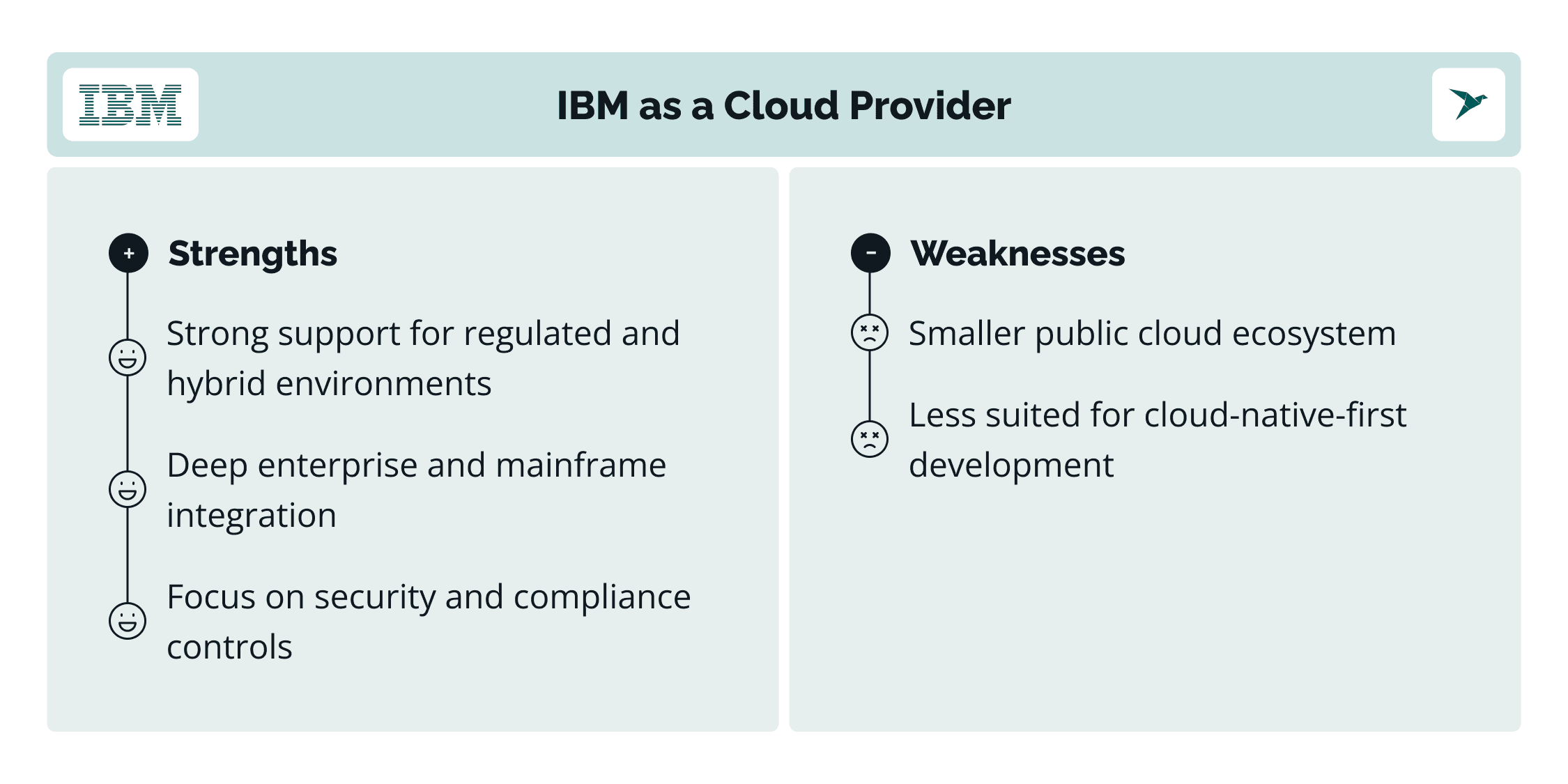

Strengths of IBM as a cloud provider

- Strong support for regulated and hybrid environments. IBM Cloud is designed to support workloads that must remain partially on-premises or in private environments. This model fits FinTech organizations that operate across legacy systems, private infrastructure, and public cloud.

- Deep enterprise and mainframe integration. IBM has long-standing experience with core banking systems and mainframe-based workloads. Its cloud services integrate well with IBM Z and existing enterprise middleware, which helps reduce migration risk for financial institutions.

- Focus on security and compliance controls. IBM Cloud offers built-in tools for encryption, key management, identity access control, and audit logging. These capabilities support compliance requirements common in financial services, including data residency and access traceability.

Weaknesses of IBM as a cloud provider

- Smaller public cloud ecosystem. Compared to AWS, Azure, or Google Cloud, IBM Cloud has a more limited marketplace of third-party services and integrations. This can slow the adoption of newer cloud-native tools.

- Less suited for cloud-native-first development. Teams building modern, cloud-native applications from scratch may find fewer managed services and less flexibility than on hyperscaler platforms. Additional customization or integration may be required.

FinTech example using IBM Cloud

BNY Mellon, one of the world’s largest custodial banks, uses IBM Cloud to support parts of its digital asset and financial services infrastructure. The platform helps BNY Mellon meet regulatory requirements while modernizing selected workloads.

IBM Cloud enables the bank to operate in a hybrid model, integrating existing core systems with cloud-based services. This approach supports security controls, auditability, and operational resilience without forcing a full shift away from established infrastructure.

For FinTech organizations with complex legacy environments and regulatory pressure, IBM Cloud often serves as a bridge between traditional systems and modern cloud operations rather than a full public-cloud replacement.

Oracle Cloud Infrastructure (OCI)

Oracle Cloud Infrastructure is often selected by financial organizations that run data-intensive, transaction-heavy systems. OCI focuses on performance consistency, database optimization, and predictable cost models, which influence how to choose cloud provider for FinTech workloads tied to core financial operations.

From a market perspective, Oracle remains a smaller player compared to AWS, Azure, and Google Cloud. Industry estimates place Oracle’s share of the global IaaS/PaaS market at around 3–4% in 2025, reflecting steady but targeted adoption rather than broad hyperscaler growth. Oracle’s cloud strategy prioritizes enterprise workloads over general-purpose cloud breadth.

Financially, Oracle’s cloud business continues to grow. In FY2025, Oracle reported over $19 billion in cloud services revenue, driven largely by Oracle Cloud Infrastructure and cloud database services. Oracle has consistently highlighted strong demand for OCI among customers migrating mission-critical and database-centric workloads.

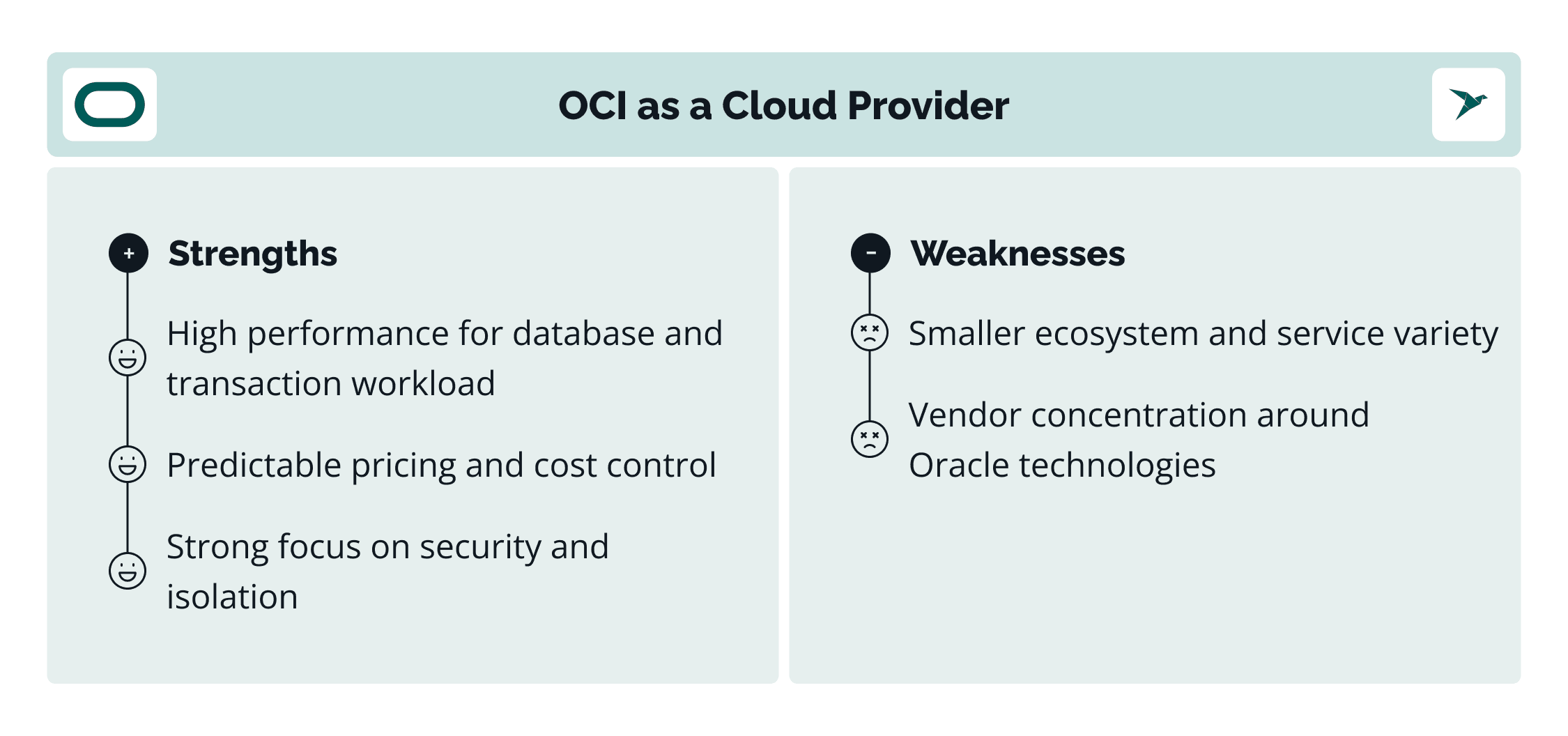

Strengths of OCI as a cloud provider

- High performance for database and transaction workloads. OCI is optimized for Oracle Database and high-throughput transaction processing. This makes it suitable for FinTech systems that depend on low latency, high I/O performance, and consistent response times.

- Predictable pricing and cost control. OCI uses a simpler pricing model with fewer variable charges compared to some hyperscalers. This helps financial teams forecast infrastructure costs and avoid unexpected spending during periods of high usage.

- Strong focus on security and isolation. OCI emphasizes network isolation, dedicated infrastructure options, and built-in encryption. These features support risk management requirements for sensitive financial data and regulated workloads.

Weaknesses of OCI as a cloud provider

- Smaller ecosystem and service variety. OCI offers fewer managed services and third-party integrations than AWS, Azure, or Google Cloud. Teams may need additional tooling for analytics, AI, or specialized cloud-native functions.

- Vendor concentration around Oracle technologies. Organizations not already using Oracle databases or middleware may face a higher adoption effort. Migrating non-Oracle workloads can require additional planning and refactoring.

FinTech example using OCI

PayPal uses Oracle Cloud Infrastructure to support parts of its payment processing and core transaction systems. OCI’s performance characteristics help handle large transaction volumes with consistent latency.

The platform supports PayPal’s requirements around availability, data security, and predictable infrastructure behavior. OCI’s database-focused architecture aligns with transaction-heavy workloads where performance stability directly affects financial operations.

Which Cloud Provider Best Supports FinTech Scalability and Global Growth?

FinTech growth depends on the ability to scale reliably across regions while meeting regulatory and performance requirements. Comparing providers at the infrastructure level clarifies how to choose provider for FinTech cloud services as platforms expand internationally.

Elastic infrastructure and managed cloud services

AWS, Azure, and GCP offer mature elastic infrastructure with extensive managed services and cutting-edge tools. Auto-scaling, managed databases, and serverless options support rapid workload growth, adapt to changing usage patterns, and help FinTech teams accelerate growth with limited operational overhead.

IBM Cloud and Oracle Cloud Infrastructure also support elasticity but with a narrower service focus. IBM emphasizes hybrid and enterprise-managed environments that work well with legacy infrastructure and regulated systems. Oracle focuses on performance consistency for database-driven workloads. These hybrid solutions fit specific growth patterns rather than broad cloud-native expansion and can help organizations avoid vendor lock-in when legacy systems remain in play.

Global coverage and data residency options

AWS and Azure provide the widest regional coverage and strong global presence, which helps FinTech companies enter regulated and emerging markets. Their regional availability supports data residency, redundancy requirements, and scaling based on regional usage patterns.

GCP operates fewer regions but maintains a strong global presence in major financial hubs. IBM Cloud and Oracle offer more limited geographic coverage, which can constrain expansion but still works for organizations operating in defined regions, supporting hybrid solutions or running under strict residency rules tied to legacy infrastructure.

Performance for high-volume financial transactions

AWS and Azure support high transaction volumes through diverse compute options, advanced networking, and managed data services. They perform well for payment processing, trading platforms, and real-time financial systems that must scale reliably as usage patterns shift.

GCP benefits from a global private network that supports low-latency distributed workloads and modern, cutting-edge tools for data processing. Oracle Cloud Infrastructure delivers strong performance for transaction-heavy and database-centric systems. IBM Cloud fits workloads that prioritize stability and integration with existing enterprise platforms, especially where legacy infrastructure still plays a central role.

Service limits, quotas, and scaling constraints

All providers enforce service limits to protect platform stability. AWS, Azure, and GCP offer formal processes to raise quotas as demand grows, which supports long-term scaling plans and helps teams accelerate growth without unexpected bottlenecks.

IBM and Oracle also apply limits, often aligned with enterprise contracts and reserved capacity models. These constraints require upfront planning but provide more predictable capacity for regulated or steady-state workloads, especially in hybrid solutions designed to avoid vendor lock-in while balancing modern cloud services with existing systems.

How Do Cloud Ecosystems and Native Services Impact FinTech Development?

Cloud ecosystems shape how quickly FinTech teams build, integrate, and evolve products. Native services, partner tools, and industry support influence development efforts and long-term flexibility. These factors matter when evaluating the top cloud service providers for FinTech and deciding how to choose FinTech cloud services provider options that align with product goals.

Financial services and industry-specific offerings

Major providers offer services designed for financial workloads. AWS and Azure provide financial services frameworks, compliance tooling, and reference architectures tailored to banking and payments.

GCP focuses more on data-driven financial use cases, while IBM Cloud supports regulated and hybrid environments common in traditional financial institutions. Oracle Cloud Infrastructure aligns closely with database-centric and transaction-heavy systems. The availability of industry-specific tooling reduces custom development and speeds delivery.

Data, analytics, and AI capabilities

Data processing and analytics drive fraud detection, risk scoring, and personalization. AWS and GCP offer mature analytics platforms and AI services that support large-scale data pipelines and machine learning workflows.

Azure integrates analytics and AI tightly with enterprise data platforms. Oracle emphasizes performance and reliability for transactional data. IBM focuses on governance, data control, and enterprise analytics. The depth of these services affects how easily teams can build and scale data-driven features.

Integration with enterprise and banking systems

FinTech products often depend on core banking platforms, identity systems, and payment networks. Azure integrates well with enterprise identity and directory services. IBM Cloud supports legacy middleware and mainframe integration.

AWS and GCP offer broad API support and integration services but may require additional configuration for older systems. Oracle Cloud simplifies integration for organizations already using Oracle databases or ERP platforms.

Partner network and marketplace maturity

Provider marketplaces extend platform capabilities through third-party tools. AWS and Azure have the largest ecosystems, with extensive offerings for security, compliance, payments, and monitoring.

GCP’s marketplace is smaller but strong in data and analytics tools. IBM and Oracle provide more focused partner ecosystems, often centered on enterprise and regulated use cases. Marketplace maturity affects tool availability, integration speed, and long-term vendor flexibility.

Let's Compare Cloud Providers in the Table

Choosing Cloud Computing Services: Tips from Techmagic’s Director of FinTech

Choosing the optimal private cloud and service provider can be challenging, especially within the FinTech sector. The goal of this article is to guide you through this process.

So, here are my recommendations as a director of FinTech at TechMagic on choosing a cloud services provider:

Tip 1: Always monitor regulatory compliance

Make sure your cloud provider fulfills industry-specific rules. Compliance with GDPR, PCI-DSS, and other norms is required in FinTech. This confirms your own data storage and handling methods match legal demands, which protects your organization from potential fines and reputation harm.

Tip 2: Prioritize security

Choose FinTech cloud service providers supplying strong encryption, data protection, and identity management. These features are crucial for safeguarding your sensitive data and preserving customer trust. Search for advanced safety measures like multi-factor authentication, encryption at rest and in movement, and complete security monitoring tools.

Tip 3: Don't neglect scalability and flexibility

Choose a provider enabling easy scaling of resources based on need. Flexibility in resource allocation can aid in managing costs and performance effectively. This is especially important for FinTech companies experiencing rapid growth or seasonal peaks in demand. Ensure the provider offers automated scaling functions and supports a wide range of instance types to fit your workload needs.

Tip 4: Build smart cost management

Implement methods to optimize cloud expenses. This includes observing usage, using cost-saving tools, and regularly examining pricing models. Consider implementing tools like AWS Cost Explorer, Azure Cost Management, or GCP’s cost calculators to gain insight into your spending, analyze costs, and identify chances for optimization.

CTOs at leading top financial app development companies highlight the crucial role of wise cost management in reaching success. Additionally, check with your cloud providers for any credits you may be eligible for.

Tip 5: Be prepared for disaster recovery and business continuity

Confirm your provider has reliable disaster recovery plans. Business continuity is vital in FinTech, where downtime can lead to significant losses. Assess the provider's disaster recovery choices, such as multi-region backups, failover mechanisms, and automated recovery processes. Regularly test your disaster recovery plan to ensure it functions effectively in case of an actual incident.

Summing Up

Choosing a cloud provider shapes how a FinTech platform scales, meets regulatory demands, and manages operational risk. The right choice depends on your product roadmap, compliance scope, and the systems you need to run and integrate, including infrastructure management. Provider strengths vary, so comparing them against your real constraints is more useful than looking for a universal “best” or chasing the best cloud provider label.

AWS offers the broadest service portfolio and global reach, but pricing can be complex and teams often face a steeper learning curve. Without tight governance, cloud spending can rise quickly, so teams often focus on cost savings and ways to optimize costs early.

Azure integrates well with Microsoft identity and enterprise tooling and supports hybrid models, but some services can become expensive at scale. Clear controls over cloud spending and ongoing tuning help optimize costs while keeping delivery speed high.

GCP stands out in data analytics and AI/ML and can be cost-effective, but has a smaller ecosystem and fewer enterprise-ready options in some areas. For teams building data-heavy features on customer data, it can support experimentation and help drive innovation while keeping an eye on cost savings.

IBM Cloud fits regulated, legacy-heavy, and hybrid environments, but has a smaller public-cloud ecosystem and more limited global reach. It’s often chosen for enterprise-grade security and regulated workloads, and in practice, many fintechs choose IBM Cloud when they need tailored solutions around legacy integration or strict governance.

Oracle Cloud Infrastructure (OCI) performs strongly for database-centric and transaction-heavy workloads with more predictable pricing, but offers fewer third-party integrations and can be most efficient when you already use Oracle technologies. For transaction platforms that prioritize stable performance and cost savings, OCI’s predictability can help manage cloud spending and support long-term planning.

Evaluate each cloud service provider based on your specific requirements, regulatory needs, and long-term goals. Engage with experts, leverage available resources, and continually reassess your cloud strategy to protect customer data, reduce operational costs, and keep room to drive innovation through tailored solutions, including emerging patterns like edge computing, where it fits.

At TechMagic, we offer cloud implementation services to assist you in making the right choice and guide you throughout the whole process. We can help you make the right provider choice and turn it into a working foundation. That includes cloud architecture planning, infrastructure buildout, secure configuration, migration support, and ongoing optimization to keep your platform compliant, resilient, and ready to scale.

FAQ

Key elements include regulatory adherence, robust security features, data safeguarding, cloud provider security, cost-effectiveness and cost efficiency, performance consistency, scalability through scalable solutions, system compatibility, strong data management, seamless integration with existing systems, and AI/ML support such as predictive analytics.

AWS generally provides competitive pricing with flexible options like pay-per-use and reserved instances, helping manage operational costs. Azure offers adaptable pricing with choices like Azure Hybrid Benefit, while GCP has transparent pricing with discounts for consistent usage that improve long-term cost efficiency.

Both support regulated workloads and deliver secure and scalable solutions. AWS offers broader service depth and fine-grained controls, while Azure often fits enterprises that rely on Microsoft identity, governance, hybrid cloud capabilities, and enterprise-grade seamless integration.

Common requirements include PCI DSS, ISO 27001, SOC 1/2, GDPR, and local financial regulations. Also, check for data residency options, encryption, audit logs, clear shared responsibility models, and strong cloud provider security backed by robust security features.

Major providers are highly available and can deliver secure and scalable solutions, but reliability depends on architecture. Multi-zone or multi-region design, failover, monitoring, and scalable solutions are usually what determine uptime.

Yes, but it can be expensive if you rely heavily on provider-specific services or a single right cloud provider strategy. Portability improves with modular design, standard runtimes, clear data export paths, and planning for multiple cloud providers.

Yes, for resilience, compliance, or vendor risk control. Using multiple cloud providers increases operational complexity, so it needs strong governance, consistent security controls, and careful management of operational costs.

AWS provides services like SageMaker for machine learning, predictive analytics, and Rekognition for AI applications. Azure offers Azure Machine Learning and Cognitive Services with strong enterprise integration. GCP is known for its AI and ML tools, including Cloud AI Platform and Cloud Vision API, and has strong support for generative AI technologies and advanced data management.